JOHANNESBURG - Everybody's mind is occupied by how long it will take for the coronavirus to let us carry on with our normal lives, and regain our savings that were decimated by it.

April and May will probably turn out to be the major turning point in the spread of the coronavirus in most developed countries.

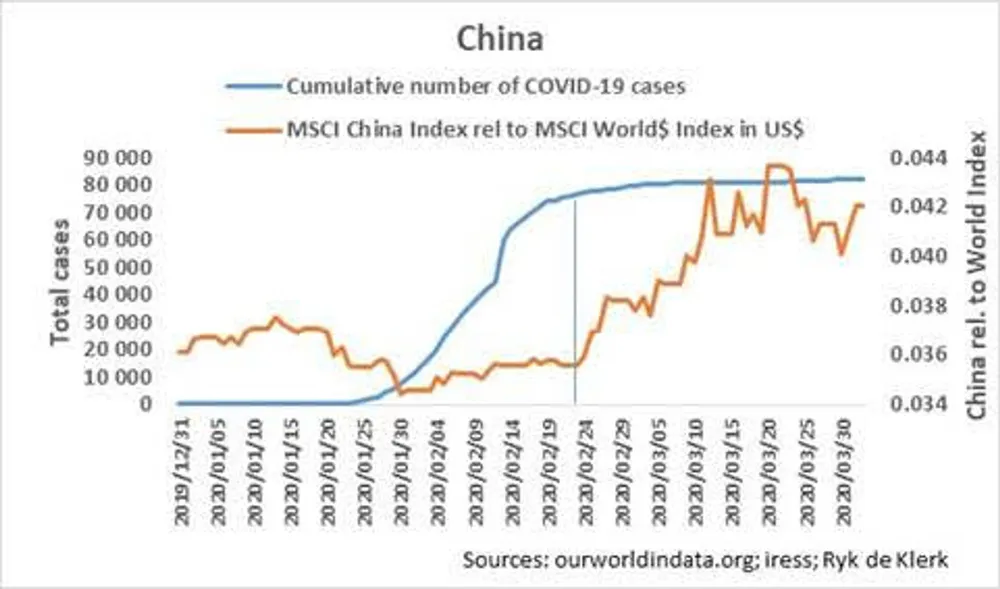

The number of new cases in South Korea and China has dropped significantly, while the curve of the total number of cases in both countries has flattened.

My analysis, based on polynomial trends, indicates that the growth in new cases in Portugal, Australia and Italy are past the peak and are slowing.

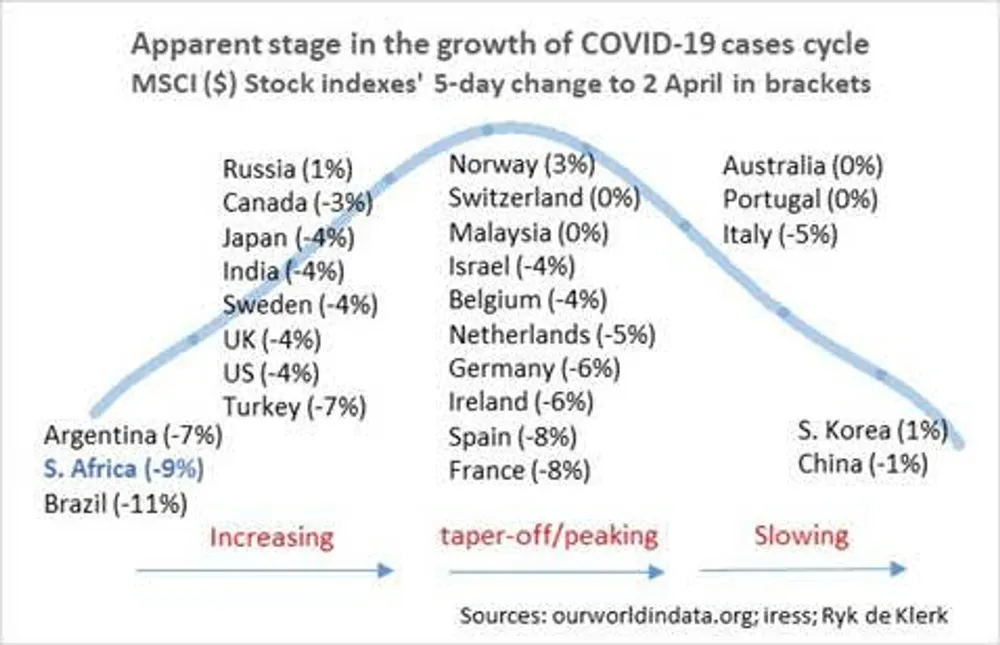

It appears that the growth curve of new cases in 10percent or 38percent of the 26 countries selected are showing definite signs of tapering off or have already peaked.

The growth trend in 11 countries or 42percent, including the UK, US, Japan, Canada and Russia is increasing.

The trend in North America (the US and Canada) is probably the most important for the world economy at this stage.

China’s experience indicates that the growth in new cases in North America will only start to taper off or peak in a fortnight meaning that the region’s economy is likely to suffer and confidence will plunge further.

It has important consequences for equity markets in the US specifically, and the mood of US investors is likely to rub-off on other global equity markets.

Again, one just has to look at the behaviour of China’s equity market compared to the developed equity markets as a whole, as measured by the MSCI World Index in terms of US dollars.

Since the outbreak of Covid-19, China underperformed in global equity markets and continued to do so until there were concrete signs that the spreading of the virus was contained.

Thereafter the Chinese stock market outperformed significantly until the uncontained outbreak in the US, and the oil price war between Russia and Saudi Arabia plunged the global economy into contraction.

The impact of where a country finds itself in the growth of the Covid-19 cycle was especially evident recently. The average return of markets in the slowing phase of the cycle over the five days to Thursday was -0.7percent, with only Italy returning a negative number.

In comparison, the average return of markets in the increasing phase amounted to a negative 4.9percent, with only the Russian market being able to produce a positive return in terms of US dollars.

The average return of markets in the taper-off/peaking cycle over the same period was a negative 3.8percent, but ranged from a positive 2percent in the case of Norway to -8percent in the case of France.

Of great concern is the fact that South America and Africa have only recently entered the increasing phase in the growth cycle of the Covid-19 cycle.

The impact thereof on equity markets was evident in their performances over the past few days.

Argentina’s stock market lost 7percent over the five days to Thursday, the South African market 9percent and the Brazilian market 11percent - all in terms of US dollars.

Although it seems that the growth in new coronavirus cases has generally peaked in Europe and is even slowing in Portugal and Italy, equity markets there will remain under pressure until the curves flatten significantly.

But Europe’s curve is way ahead of North America, and European equity markets could outperform their North American counterparts sooner rather than later, as lockdowns will end sooner in Europe.

If the US manages to flatten the growth in Covid-19 cases over the next two to three weeks, the chances are good that April/May could herald the worst point in the current crisis globally as Europe will by then have joined China and South Korea in an effective flat Covid-19 curve.

South Africa and the South American markets are behind the curve compared to others.

It is, therefore, likely that the South American markets will continue to under-perform compared to other world equity markets, and specifically equity markets in developed economies, until such time when South Africa, Brazil and Argentina manage to start to reverse the awaited up-trend in new cases.

Perhaps it is then best for South Africa to extend the lockdown.

Although the JP Morgan Composite purchasing managers’ index fell by the most since the 2008/9 global financial crisis, indicating that global economic growth is contracting by about 2percent year-on-year, global equity markets have not revisited their valuation lows of 2008/9, but a fortnight ago South African markets did.

Global stock markets are already in value territory, but some downside risk remains as the markets might only bottom three months after the sharp contraction - as they did in early 2009.

The scary thing is that the curve of total deaths caused by Covid-19 in China only started to flatten about 14 days after the curve of total cases started to flatten.

The news headlines are likely to focus on the deaths and suppress confidence, especially consumer confidence.

Although US consumer confidence fell by 10percent in March month-on-month, it is still a far cry from more than 70percent in 2008.

Consumer confidence is crucial for US equity markets, so the next two to three months will be a very bumpy ride to say the least, but the longer-term picture for US stocks looks good - and therefore for stocks globally.

I handle the market in the same way as how I treat anything that I buy from shelves in these times: it could be infected and cost me dearly.

Ryk de Klerk is analyst-at-large. Contact rdek@iafrica.com. His views expressed above are his own. He has no direct interest in any company if mentioned in the article. You should consult your broker and/or investment adviser for advice.

BUSINESS REPORT