File image: IOL File image: IOL

JOHANNESBURG - Bloodletting and extreme volatility of stocks in the JSE-listed real estate sector caused huge panic selling and massive financial problems for pensioners, savers and retirement funds.

A SENS announcement by Growthpoint (GRT) on April 1 caught my attention. The company announced that Prudential Investment Managers (South Africa) has increased their beneficial stake in Growthpoint to 5.2 percent of Growthpoint’s total issued ordinary shares. According to Growthpoint’s website, Prudential held 4.1 percent of Growthpoint at the end of December last year.

Is this where the smart money is going?

The draw down (price fall) of the JSE SA Listed Property Index over five years to the end of March was 66 percent and is the worst draw down in listed property that I have on record.

Although the constituents and the make-up of the FTSE/JSE SA Listed Property Index have changed over the years, the draw down is even worse than the 51 percent draw down of the old Property Unit Trusts Index over the five years to August 1998 during the 1998 economic crisis in Russia which has hit South Africa very hard.

Growthpoint’s share price held up reasonably well with a draw down of 55percent over the five years to the end of March this year.

I view this Real Estate Investment Trust (Reit) as a blue chip in the SA Listed Real Estate sector and due to the company’s history spanning many years, use it as my benchmark for the sector.

It is important to understand the reasons for the chaos in listed Reits.

Before the Covid-19 crash, South African bonds reflected the market’s expectation of a cut in South Africa’s credit rating to junk status by Moody’s. This resulted in South Africa 10-year government bonds trading at about 150 basis points higher than they would, in light of South Africa’s corresponding credit rating at that stage.

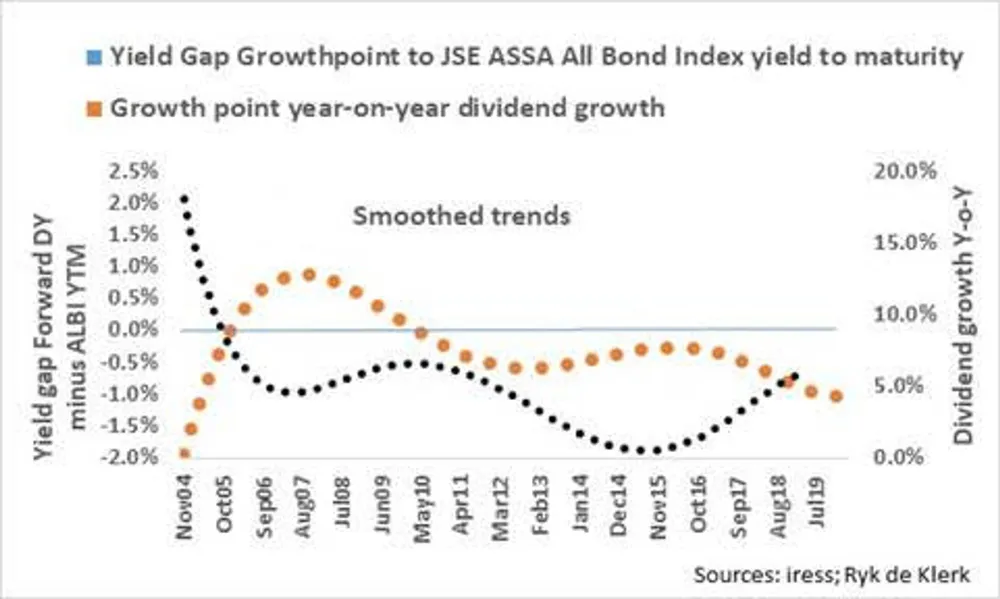

The relationship between Growthpoint’s one year forward dividend yield and the yield to maturity (YTM) of the JSE Assa All Bond Index (Albi) is linear. The opening or closing of the yield gap can be explained by the growth rate of Growthpoint’s dividend.

When the growth rate accelerates, the gap between the Albi yield and Growthpoint’s forward dividend yield increases and vice versa, the gap narrows when Growthpoint’s dividend growth slows down. When the YTM of the Albi changes by 100 basis points, say from 8 percent to 9 percent or from 8 percent to 7 percent, the capital value of Albi change by around 6.5 percent. This change per 100 basis points is also known as the modified duration.

If the forward dividend yield of Growthpoint increases by 100 basis points, say from 8 percent to 9 percent, the share price of GRT falls by 11 percent, while if the forward dividend yield drops by 100 basis points, from 8 percent to 7 percent, Growthpoint’s share price increases by 14 percent.

So, on average the share price changes by 12.5 percent by a 100 basis point change in the forward dividend yield. Growthpoint’s modified duration therefore is around 12.5 percent.

At the height of the crash on March 23/24, which resulted in a major sell-off in emerging market bonds, the yield of the Albi jumped to around 12.5 percent from 9.6 percent at the end of February. The 290 basis point jump, therefore, resulted in a loss of 17.3 percent in capital value of the Albi.

In light of the linear relationship of the Growthpoint’s forward dividend yield and the Albi yield, one would have expected a fall of about 32 percent in the share price. The share price fell by 39 percent and, if the interim dividend of 106c paid last week was excluded, it meant that the share price fell by 45 percent.

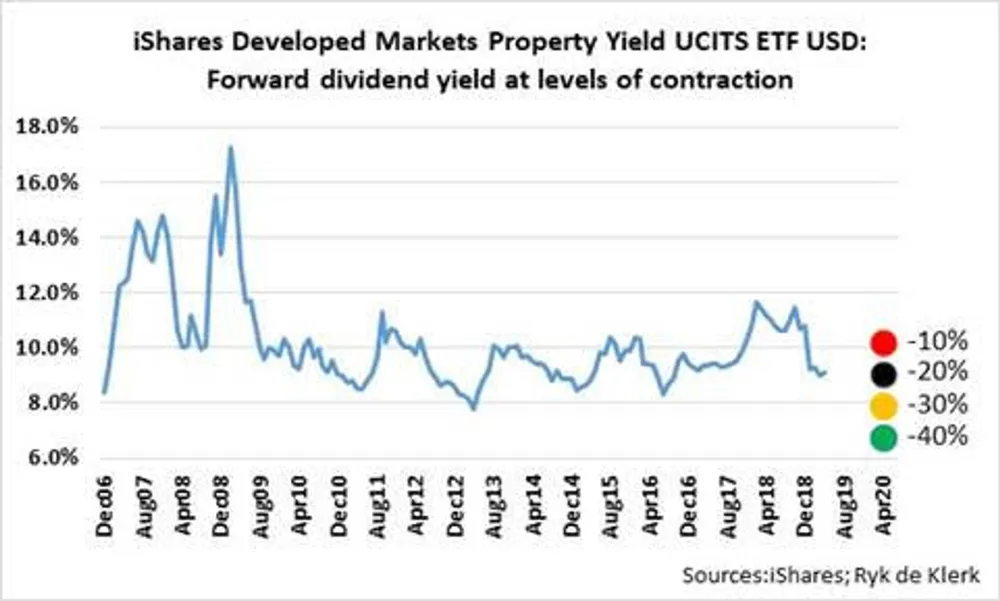

In comparison, the iShares Developed Markets Property Yield UCITS ETF USD (Dist.) which seeks to track the performance of FTSE EPRA/Nareit Developed Dividend+ Index composing of listed real estate companies and Real Estate Investment Trusts (Reits) from developed countries, excluding Greece, fell by 36percent in terms of US dollars.

What it means is that on March 23-24, the market anticipated a knock of about 13percent in Growthpoint’s dividend over the next 12 months. At the close on Thursday, Growthpoint’s share price had recovered by some 42 percent from the lows in late March, while the Albi yield dropped by 150 basis points to 11.1 percent resulting in a gain of 10.3 percent over the same period. The iShares Developed Markets Property Yield UCITS ETF recovered by 31 percent.

Nearly 60 percent of the iShares Developed Markets Property Yield UCITS ETF’s holdings are in North America (57 percent in the US), followed by 11 percent in Europe, 8 percent in Japan, 7 percent to Hong Kong and 5 percent in the UK.

After the meltdown from 2007 to 2009 the average forward dividend yield of the iShares Developed Markets Property Yield UCITS ETF was 9.6 percent with a standard deviation of nearly 1 percent. At this stage it appears that the net asset value or price of the ETF anticipates dividends to fall by between 15 percent and 20 percent over the next 12 months. As I pointed out earlier, the outlook for Growthpoint is highly dependent on dividends and South African bond yields, specifically that of the Albi.

Assuming that the gap between Growthpoint’s 12-month forward dividend yield and the yield to maturity of the Albi has closed, it appears that the market is expecting a decline of about 30 percent in Growthpoint’s dividend over the next 12 months.

Against the backdrop of the lockdowns globally, it is possible that the fallout could result in an even deeper contraction in dividends globally as well as in Growthpoint’s case.

The major determining factor in where Growthpoint’s share price and the listed real estate sector as a whole are going is where the Albi yield is heading. That, per se, is highly dependent on the outlook for emerging market assets and especially emerging market bonds. Old Mutual and some offshore fund managers recently indicated that the South African bond market in particular looks attractive and are offering value.

Declining bond yields are likely to be highly supportive of listed Reits prices on the JSE.

The risks remain high though. As alluded to in my article last Monday, global markets face a bumpy ride in coming months. We might even see a retest of the lows in March.

In the case of Growthpoint and the SA Listed Property sector as well as the global Reits, the markets will at some stage begin to change focus on a more positive outlook post the unprecedented environment caused by Covid-19. At this stage I am comfortable to view high-quality Reits with solid balance sheets as long-term annuity investments.

One thing is certain. The developments in the markets over the past few months have shown that, contrary to previous beliefs by some asset managers and financial advisers, bonds and Reits are not risk-free investments.

Ryk de Klerk is analyst-at-large. Contact rdek@iafrica.com. His views expressed above are his own. He has a direct interest in Growthpoint. You should consult your broker and/or investment adviser for advice.

BUSINESS REPORT