A nurse wears protective gear in a ward dedicated for people infected with the new coronavirus, at a hospital in Tehran, Iran, Sunday, March 8, 2020. With the approaching Persian New Year, known as Nowruz, officials kept up pressure on people not to travel and to stay home. Health Ministry spokesman Kianoush Jahanpour, who gave Iran's new casualty figures Sunday, reiterated that people should not even attend funerals. (AP Photo/Mohammad Ghadamali) A nurse wears protective gear in a ward dedicated for people infected with the new coronavirus, at a hospital in Tehran, Iran, Sunday, March 8, 2020. With the approaching Persian New Year, known as Nowruz, officials kept up pressure on people not to travel and to stay home. Health Ministry spokesman Kianoush Jahanpour, who gave Iran's new casualty figures Sunday, reiterated that people should not even attend funerals. (AP Photo/Mohammad Ghadamali)

JOHANNESBURG - The South African government is lauded for its tremendous success in pushing out the Covid-19-curve by at least two weeks by acting timeously and appropriately, and flattening the curve relative to the experience of China’s and some other major economies.

As a nation we have enough in our arsenal to survive the current crisis caused by the coronavirus and to set the country on a steady and strong growth path.

South Africans have the will to rise again, and the best example is the sober approach of Cosatu. They have had enough of corruption and malfeasance at all levels of the government, state-owned enterprises (SOEs) and the private sector.

What they want is a growing economy that will ensure that job losses are kept to the minimum.

They are prepared to use their deferred income - retirement funds - to recapitalise highly indebted SOEs decimated by corruption and malfeasance and invest in the private sector to get the economy going. More importantly, they want their off-spring to get a job one day. Despite heavy criticism, from the Eskom crisis to the current crisis, an alternative to Cosatu’s proposals - accepted by President Cyril Ramaphosa - is yet to come to the fore. Their proposal of the effective reintroduction of prescribed assets where all retirement funds, life assurance industry and assets managed by the PIC invest at least 10 percent of their assets in government bonds makes sense.

In my opinion, the time has arrived for inward investing by the savings sector by lowering the Regulation 28 limits of investing offshore and to ensure that the repatriated funds are productively employed in the economy through the prescribed asset mechanism. What people and economists forget or would like to forget is that every rand savings leaving the country is one rand less for available investment or spending in this country. Although the offshore funding doors have closed on us, we need not be a beggar country or nation.

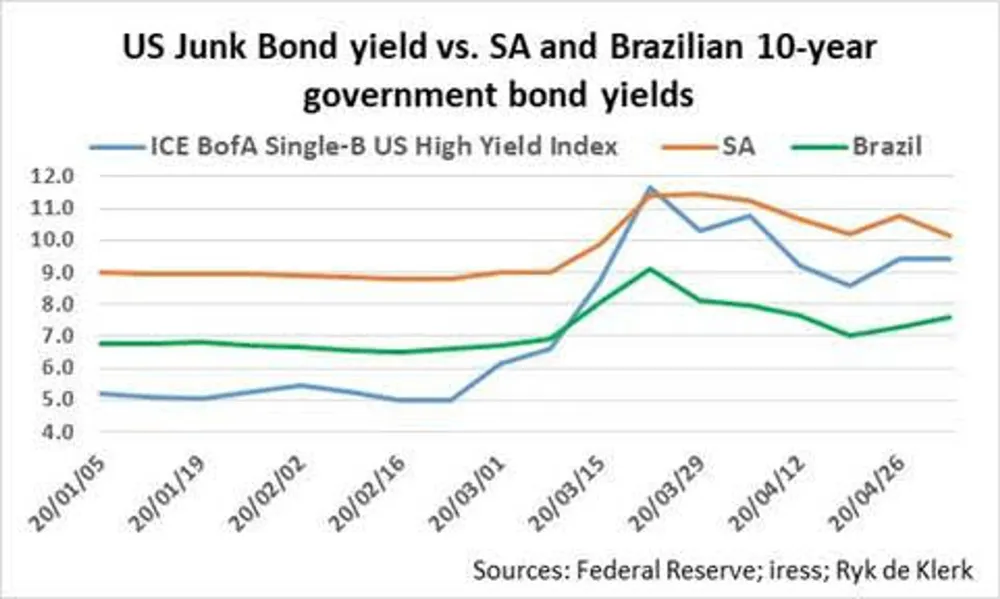

Until the fourth quarter of 2018, South African bonds as measured by the 10-year government bonds traded at a premium to Brazilian bonds and reflected the corresponding sovereign credit ratings differential, where South Africa was still investment grade according to Moody’s.

As things started to fall apart in South Africa with Eskom’s woes and the resulting devastating impact on the economy, SA bonds traded on par with Brazilian bonds until the second quarter last year. The down rating of South Africa was well telegraphed and the fallout from the JPMorgan Global Government Bond Index anticipated in advance as the gap between SA bonds yields and Brazilian bond yields opened in favour of the latter.

South African and Brazilian bonds are now displaying similar characteristics of US junk bonds. The two sovereign bonds will therefore by default benefit when the US economy stabilises and the capital risk of junk bonds recedes.

It does seem that the markets have treated South African government bonds too harshly, but are they wrong? The South African government is lauded for the announcement of a stimulus of between R500billion and R800bn to bolster the economy as soon as the lockdown ends. S&P Global Ratings is not impressed with the number and so am I, as it will only put the country back to where it was pre-coronavirus crisis. Cosatu calls for at least R1trillion.

The red flags are already there. We are all aware of the SAA disaster and the Land Bank’s default on its loans. The bond market is telling us all is not well at Eskom and Airports Company South Africa (Acsa), as their bond yield spreads to South African government bonds over corresponding maturities have widened since the first week of April.

Only the National Treasury and the top management of the two SOEs will know what the current financial situation is and how it will pan out in the current 2020/21 financial year.

Gleaning from how the economy performed in Acsa’s 2019/20 financial year, it is likely that the SOE’s operating profit before interest and tax hardly reached breakeven, and they probably burnt all their cash - so to speak.

With a pre-interest cost base of nearly R5bn and minuscule turnover due to the lockdown, the SOE is in danger of reporting a loss before interest and tax of up to R5bn.

In addition, in light of the massive crunch in real estate investment trust share prices, I will not be surprised if the value of Acsa’s investment property portfolio will be slashed down to the valuation as per the 2014/15 annual financial statements. Yes, an impairment of more than R2.5bn. Total borrowings could sky-rocket to more than R14bn at the end of the 2020/21 financial year from just more than R6bn at the end of the 2018/19 financial year.

The bottom-line is that Acsa is in grave danger of entering my so-called debt-death cross where total borrowings net of cash exceeds shareholders’ interest. But that is not where it ends. Even if things return to normal in the 2021/22 financial year, the interest burden on the borrowings could be such that the SOE’s profit before tax and interest will be a fraction of interest paid. Acsa will need a serious capital injection to avoid being placed under business rescue. Cosatu’s plan is a solution.

It is impossible to even grasp what is going on at Eskom, and how things will pan out by the end of the 2020/21 financial year. What one does know is that the SOE’s profit before interest, tax and depreciation will be under strain due to the impact of the lockdown on Eskom’s base load, due to the suspension of mining operations and manufacturing.

The SOE will also receive a boost after it won the high court appeal against the National Energy Regulator of South Africa (Nersa), which prevented Eskom from recovering R27bn in costs. Eskom will hike tariffs.

The outlook for Eskom beyond the current financial year is highly uncertain, as due to the massacre of state finances by and large as a result of the Covid-19 crisis, the government might not be in a position to provide the financial support as envisaged. A serious capital injection will be required. Cosatu’s plan specifically addresses that.

The other SOEs are probably in similar financial difficulties.

Edward Kieswetter, the commissioner of the SA Revenue Service (Sars), last week said that the loss of revenue from VAT, excise duties, import duties and PAYE in April amounted to more than R30bn, yes, more than R1bn per day, and it will get worse. Period.

This is not the time to settle political scores. We need not be a beggar country or nation and this is not the time to negotiate when, where and how things will be tackled. The time to act is now!

Ryk de Klerk is analyst-at-large. Email him at rdek@iafrica.com. His views expressed above are his own. You should consult your broker and/or investment adviser for advice.

BUSINESS REPORT