The end of the bear market in developed market bonds is in sight. File Image: IOL

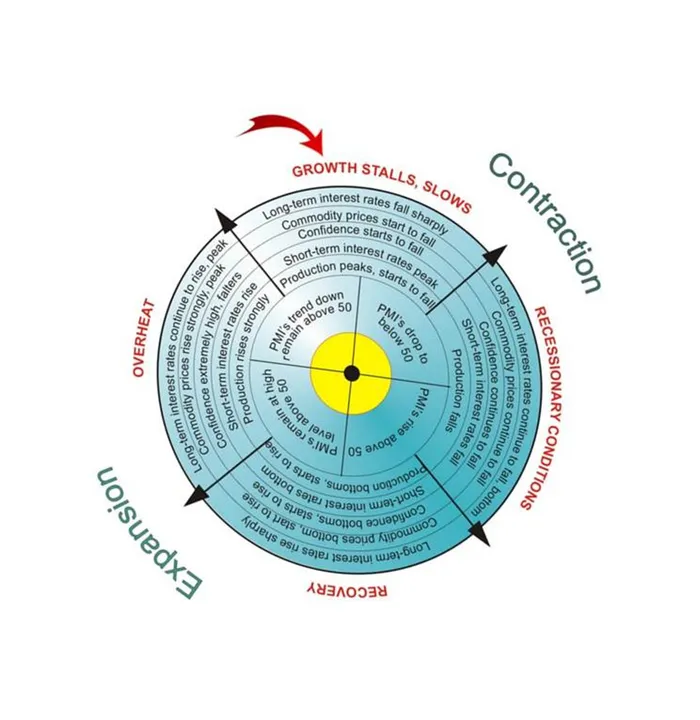

THERE ARE are definite indications that global economic growth is slowing. The first indications availed themselves as the yields on some longer-dated bonds dropped below the yields of shorter-dated bonds – yes, inverted or flat yield curves. But where lie the opportunities?

The end of the bear market in developed market bonds is in sight. Bonds, as measured by the FTSE G7 Government Bond Index, which is tracked by the iShares Global Gov. Bond UCITS ETF USD (Distr.), lost 17 percent since December 2020 as bond yields climbed. Firstly, as a result of the global economy recovering from the coronavirus and its mutants and secondly, the onset of the Russian/Ukrainian conflict.

The massive sanctions against Russia saw the US Federal Reserve and other central banks hiking their official lending rates to quell the spike in inflation rates caused by the jump in oil prices and the scarcity of goods and labour.

The change in the price of crude oil from the same month a year ago is a main contributing factor in the level of the US Consumer Price Index inflation rate.

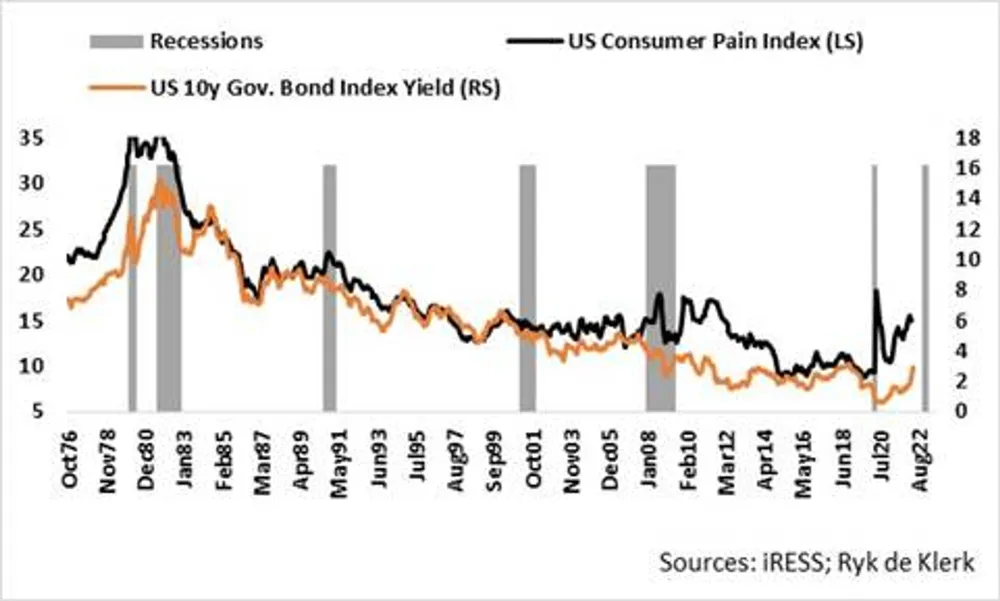

My US Consumer Pain Index measures consumers’ discomfort by adding the 30-year mortgage bond rate to the inflation rate and the unemployment rate as well. It is currently approaching the highs during and immediately after the Global Financial Crisis in 2008/09, as well as the high at the peak of Covid-19. In both instances, the US economy slid into a recession.

Inflation peaked at the end of March at about 8 percent. If the oil price remains unchanged at current levels for the next 12 months, we will see inflation drop steadily to 3.5 percent in the third quarter and drop further to 2 percent in the first quarter of next year.

The Fed’s tapering and planned hikes in the repo rate in the case of a steady oil price at current levels could choke the economy, but a recession in coming quarters may be averted, though. The US Consumer Pain Index will, however, remain elevated as mortgage rates are likely to remain high, and unemployment will increase as economic growth fizzles out. Consumer confidence will be eroded while the stock market will take the pain.

I think we all agree that, in light of what happened globally over the past two years, the world is a more risky place. Significant increases in the oil price will tilt the US into a recession. And other Black Swans events will occur caused by geopolitical and viral threats that could push oil prices higher.

Expect a more aggressive stance by the Fed if the oil price jumps $25 (R364) from current levels, as Inflation could then be about 6 percent at the end of the current quarter. Inflation will remain at about 5.5 – 6 percent through the end of the third quarter, then drops steadily to 3 percent by the end of the first quarter of next year. Yes, an outright recession can be expected in these circumstances.

You can count on a very aggressive stance by Fed and a very deep recession if the oil price jumps $50 overnight from current levels and remains there in the ensuing 12 months. Inflation will remain around at 7 percent until the end of the year and then subside to 4 percent by the end of the first quarter year.

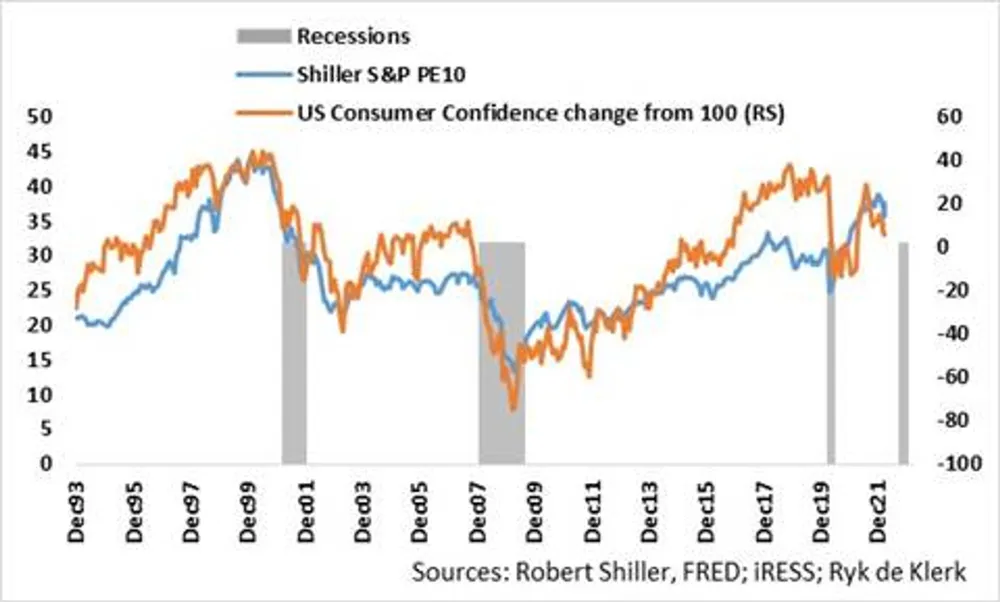

Consumer confidence will crash, and in light of the close relationship with Robert Shiller’s cyclically adjusted PE10 (price earnings ratio is based on average inflation-adjusted earnings from the previous 10 years), the US and global stock markets will tank. The Consumer Confidence Index took four years to regain the pre-global financial crisis levels.

Black Swan events (unpredictable events that have major impacts) and viral threats may cause the Consumer Pain Index to overshoot on the upside.

But what are the best defensive strategies against Black Swan events and viral threats?

Although defensive stocks (consumer staples, communication, healthcare) tend to be more stable in economic downturns as they provide consistent dividends and stable earnings due to inelasticity in demand, they are also prone to major sell-offs in stock markets as a result of Black Swan events. They do tankless than other stocks when consumer confidence crashes. Steer clear from emerging market assets except for dual-listed offshore defensive stocks.

In these cases of crises, the Fed and other major central banks will have to resume quantitative easing, yes, by buying longer-dated bonds and forcing long rates down to close to zero. The US yield curve is likely to drop by more than 150 basis points.

But what will happen to the price of the JSE-listed 1nvest Global Government Bond ETF that tracks iShares Global Gov. Bond UCITS ETF USD (Distr.) if the yields of its underlying assets jump by 100 basis points overnight due to a Black Swan event? As bond yields fall, bond prices increase and vice versa.

The weighted average effective duration of the ETF is about 8.5. The weighted average maturity of the bonds is about 10 years. The ETF’s country weighting is approximately 25 percent in the Euro Area, 50 percent in the US and Canada combined, 19 in Japan and 5 in the UK. What it means is that in normal circumstances, should the yields of the ETF’s underlying assets increase by 100 basis points, the capital loss will be 8.5 percent.

However, the Bank of Japan’s (BOJ) target is a 50-basis point band around the BOJ’s target of zero percent to keep interest low to stimulate the economy. The BOJ’s huge presence in the Japanese government bonds ensures that the target is met.

What it implies is that with the 10-year yield of Japan now at the upper end of the target, a 100 point increase of the 1nvest Global Government Bond ETF will be a 5.8 effective yield, meaning that the price of the index will fall by a mere 5.8 percent.

In the case of a 100 basis point drop in first world market yields, the gain in price will be about 6.6 percent as the fall in Japan’s 10–year government bond yield will be limited by 50 basis points from current levels.

Yes, the current stage in the global business cycle favours G7 bonds. G7 bonds offer uncorrelated returns and protection against Black Swan events as well as rand depreciation against hard currencies. Further upside in yields is probable, but capital losses are likely to be far more limited than equities, especially economic cyclical stocks.

Ryk de Klerk is analyst-at-large. Contact rdek@iafrica.com. He is not a registered financial advisor and his views expressed above are his own. You should consult your broker and/or investment advisor for advice. Past performance is no guarantee of future results.