Explore why a TFSA can outperform other investment options, how to make the most of your contributions, and what strategies can help you maximise your long-term growth.

Image: File photo.

In his Budget Speech, the Minister of Finance announced an increase in the annual Tax-Free Savings Account contribution limit from R36,000 to R46,000 - the most significant boost to this allowance in years, and a timely reminder of just how powerful this vehicle can be.

When used properly, it can deliver returns that are completely tax-free, not just today but for life.

While TFSAs are flexible, their true potential lies in long-term investing, allowing your capital to compound over decades. In this article, we’ll explore why a TFSA can outperform other investment options, how to make the most of your contributions, and what strategies can help you maximise your long-term growth.

It’s important to understand the non-negotiables:

Although a TFSA allows withdrawals at any time, it is not intended as an emergency fund. The real value comes from leaving it invested for as long as possible and letting compounding do the heavy lifting. Once money is withdrawn, that portion of your lifetime limit is gone for good.

Let’s explore why a TFSA can outperform other investment options, how to make the most of your contributions, and what strategies can help you maximise your long-term growth.

Should I contribute to a TFSA or a Retirement Annuity?

The key difference:

This means a RA contribution only adds real value if the tax saved today is greater than the tax paid later.

As a general guideline, investors in lower- to moderate-tax brackets, often around 31% or below, may benefit from prioritising TFSA contributions first. At these levels, the immediate tax deduction available through an RA is less significant, while the TFSA allows capital to grow tax-free over long periods of time.

There’s also flexibility to consider:

There is no one-size-fits-all answer. The right balance depends on your income, tax rate, and long-term goals. This is where proper planning matters.

*Some providers may have platform limitations on offshore exposure.

Why invest in a TFSA rather than a flexible investment?

To understand the real power of a TFSA, let’s compare it to a flexible investment. This removes the flexibility constraints the RA has.

Assumptions:

This means a RA contribution only adds real value if the tax saved today is greater than the tax paid later.

As a general guideline, investors in lower- to moderate-tax brackets, often around 31% or below, may benefit from prioritising TFSA contributions first. At these levels, the immediate tax deduction available through an RA is less significant, while the TFSA allows capital to grow tax-free over long periods of time.

There’s also flexibility to consider:

There is no one-size-fits-all answer. The right balance depends on your income, tax rate, and long-term goals. This is where proper planning matters.

*Some providers may have platform limitations on offshore exposure.

To understand the real power of a TFSA, let’s compare it to a flexible investment. This removes the flexibility constraints the RA has.

Assumptions:

Same contribution. Same return. A R1.54 million difference, purely due to tax.

Image: Supplied.

How should you invest in your TFSA?

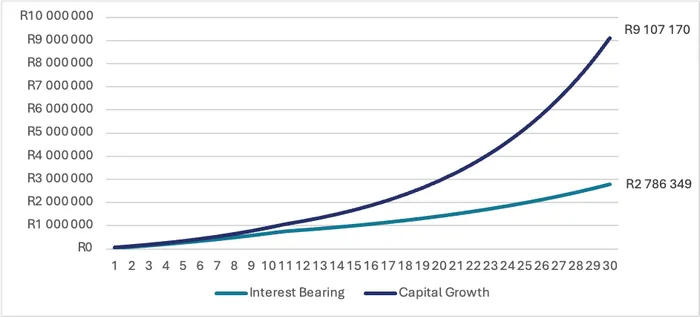

As the biggest benefit of a TFSA is the savings on capital gains tax, the best way to maximise the growth is to invest in high-growth assets. This typically means a portfolio with high exposure to equities, especially offshore equities. Typically, this type of portfolio returns at least 12% p.a.

So, why is your bank offering you a TFSA? Well, because the tax benefit of not paying interest on your capital is also substantial. However, a tax-free return of 7% is still less than a tax-free return of 12%. It can mean a difference of R5.4 million after the 30-year period. Therefore, maximising the return you can get is essential to long-term performance.

To understand the real power of a TFSA, let’s compare it to a flexible investment.

Image: Supplied.

Is there a material difference between contributing R3,833.33 p.m. at the start of each month or R46,000 every year in March?

Yes, there is a marginal mathematical advantage to contributing R46,000 at the start of the tax year rather than R3,833.33 per month. With annual contributions at the start of the year, more money is invested earlier, allowing compounding to get a head start.

Over a 30-year period, the investor who contributes annually upfront ends up with R453,748 more.

However, here’s the part that matters more than the spreadsheet. If contributing annually means the money sits in your bank account and somehow “disappears”, then the strategy has already failed. For many investors, a monthly debit order is far more effective than relying on discipline and timing a large lump sum once a year.

Consistency beats optimisation.

A TFSA that is funded every month, every year, will always outperform a TFSA that was supposed to be funded annually but never quite gets around to it.

If a monthly debit order is what ensures the contribution actually happens, then that is the better strategy. Always.

Investing in a TFSA isn’t just about saving, it’s about supercharging your wealth over time. By keeping your funds invested, prioritising high-growth assets like equities, and contributing consistently, you can take full advantage of the tax-free benefits.

Speak to your financial planner today to ensure your TFSA is working as hard as possible for your financial future, because when it comes to compounding, every year counts.

Liza Brink is an Associate Investment Analyst who supports the investment team through manager research, fund analysis and performance attribution.

Liza Brink is an Associate Investment Analyst who supports the investment team through manager research, fund analysis and performance attribution.

Image: Supplied.

PERSONAL FINANCE