Claims history is one of the factors affecting car insurance premiums.

Image: Freepik

Two South Africans can insure the same make and model of car and still end up paying very different monthly premiums, sometimes by hundreds of rands.

This is because insurers do not price policies based only on the vehicle. They also assess the risk profile of the driver and how the car is used.

“People often assume car insurance is priced mainly on the car,” says Ernest North, co-founder of car insurance provider Naked. “But in reality, insurers are trying to estimate two things: how likely you are to claim, and how expensive that claim is likely to be.”

This means that even identical cars can attract different premiums depending on who is driving them. However, the car does make a difference. The highest accepted car insurance premium recorded by Hippo was R61,817 per month. This was for a Mercedes-AMG G-Class G63.

Insurers consider a range of factors when assessing risk. These include age, driving experience, claims history, how long a person has been insured, where the car is used and parked, and credit record.

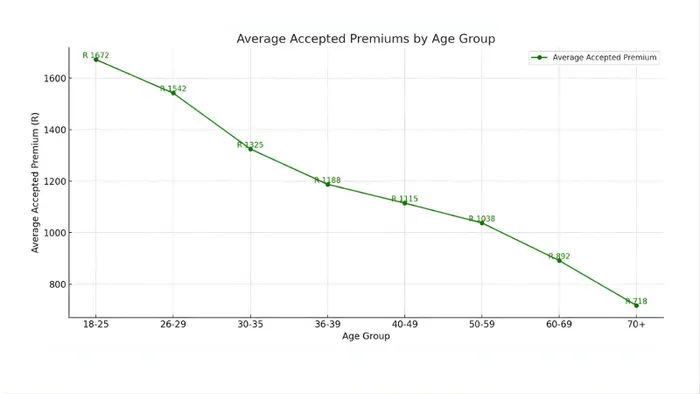

Hippo provides some data as to how age can affect premiums:

Different insurers weigh factors differently, which is one reason quotes can vary across providers. “Insurers don’t price a Toyota Corolla in isolation,” says North. “They price a Toyota Corolla driven by you, in your context.”

For example, a driver with a long licence history, no recent claims and secure parking is likely to pay less than someone with limited driving experience, a recent claim and higher-risk parking conditions.

A long-held view is that women pay less in insurance than men, but Hippo.co.za’s data shows that women pay R277 more on average on their monthly premiums.

Location also matters. Polokwane in Limpopo has the highest average premiums per month for the VW Polo at R1,666, Hippo says.

They’re followed by Northwest (Mahikeng) and then Gauteng (Johannesburg). The lowest average premium among the popular vehicles is in Western Cape (Cape Town) for the Toyota Corolla at R913.

Age premiums accepted by age group.

Image: Hippo

The excess – the amount a driver pays when claiming – also affects the monthly premium. A higher excess generally reduces the premium, while a lower excess increases it.

“The key is to choose an excess you can realistically afford,” says North. “A lower premium can look attractive, but not if it leaves you stuck when you actually need to claim.”

North adds that some policies include additional excesses under certain conditions, such as for younger drivers, night driving or early claims in a policy.

“Those add-ons can stack up and significantly increase what you pay when something goes wrong,” North says.

Premiums can also differ based on what is included in the policy.

Optional extras such as car hire or credit shortfall cover can increase the cost, while differences in cover levels and excess structures can make quotes appear similar when they are not.

“People often compare prices without comparing what’s included,” says North. “The right question isn’t only ‘what does it cost?’ It’s ‘what am I covered for, and what would I pay if something goes wrong?’”

Many online tools provide only an estimated premium, with final pricing confirmed after additional information is provided. Comparing quotes on a like-for-like basis, including cover, benefits and excess, is the most reliable way to assess whether a policy offers value.

IOL BUSINESS