Prices are rising, demand is returning, and banks are lending more freely when it comes to property.

Image: Pexels

South Africa’s property market is starting to move again – but not in the same way everywhere.

Prices are rising, demand is returning, and banks are lending more freely, according to BetterBond data. But beneath that recovery, the market is splitting, with some regions gaining value and others slipping back.

At a national level, the data is turning positive.

For the first time in more than a year, house prices are rising in real terms, according to BetterBond, pointing to a market that is moving beyond interest rate pressure.

According to data from BetterBond’s latest Property Brief, house prices have reached a milestone with positive real inflation recorded for both first-time buyers and repeat buyers.

This is the first such occurrence since before the last quarter of 2024. “Adjusted for inflation, this means a 1.9% increase for all buyers and 0.2% for new buyers,” says Stephan Potgieter, CEO of BetterHome Group Mortgage Origination and BetterBond.

Statistics South Africa’s Residential Property Price Index most recent Residential Property Price Index for October showed that residential property prices rose 6.8% year on year in October 2025.

This means that a home valued at R1 million a year earlier would now be worth roughly R1.07 million, according to Statistics South Africa’s data.

Potgieter said “encouragingly, record prices were reported during the first two months of this year – R1.66 million for all buyers and R1.35 million for first-time buyers”. Lower borrowing costs are feeding into that shift, BettaBond’s report shows.

The prime lending rate has declined by 1.50 percentage points since September 2024, reflecting improved fiscal confidence, its report stated. Home loan applications are up 3% year-on-year in the first two months of 2026 and more than 18% higher than late 2023 levels, according to BetterBond.

“Stronger income growth is having an impact on improved affordability, particularly among buyers aged 51 to 60. This group now earns an average annual income equal to 58% of their typical home purchase price, reflecting a 36% increase since 2022,” said Potgieter.

Overall, affordability has improved at an average annual rate of 5.1% across all buyers. These trends are consistent with data from Statistics South Africa, which indicates that formal sector incomes have risen by an average of 4.3% per year over the past four years,” Potgieter added.

New data from Statistics South Africa shows that while the Western Cape continues to dominate the country’s largest housing markets, Limpopo recorded the fastest house price growth in South Africa.

But that recovery is not playing out evenly. In parts of Johannesburg, prices are still under pressure due to service delivery challenges, according to BetterBond.

“There has been a real year-on-year decline of 8.7% in house prices in Johannesburg’s north-western suburbs. Although not as pronounced, there has been a drop in average house prices in the south-eastern suburbs as well,” said Potgieter.

By contrast, the Western Cape continues to lead on price performance, the data shows.

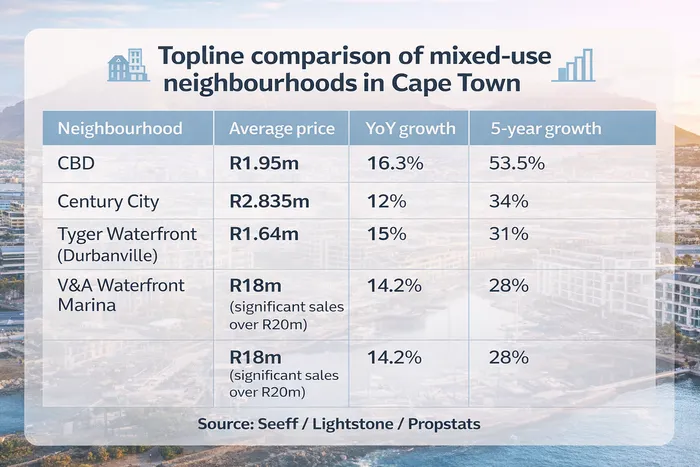

Mixed-use neighbourhoods are generally highly sought by investors for high rental demand and stable yields.

Image: ChatGPT with Seeff data

“The Western Cape continues to outperform in terms of house prices, recording the highest average price of R2.27 million alongside strong nominal growth of 8.1%, underpinned by semigration trends and sustained demand,” said semigration.

Properties in the province are also selling faster than elsewhere.

“Underscoring the ongoing demand as a result of semigration and other pull factors, houses in this province also have the shortest average selling time – spending around six weeks and two days on the market,” said Potgieter.

Statistics South Africa noted that among the country’s largest property markets, the Western Cape recorded price growth of 9.1%, meaning a R1 million home a year ago would now be worth roughly R1.09 million.

Demand is increasingly concentrated in specific areas, particularly mixed-use neighbourhoods, according to Seeff Property Group.

Prices in leading Cape Town nodes have increased by between 30% and 50% over five years, with year-on-year growth of between 12% and 16%, outperforming both the broader Cape Town average of 9.1% and the national average of 6.6%, based on Statistics South Africa data.

Among the country’s largest property markets, the Western Cape recorded price growth of 9.1%, meaning a R1 million home a year ago would now be worth roughly R1.09 million, according to Statistics South Africa.

Cape Town outperforms Joburg in house price growth.

Image: ChatGPT

Statistics South Africa lists growth in the metro at 10% for October year-on-year.

Helga Clemo, licensee for Seeff Century City says century City Prices are up by over 20% over the last two years.

“Sellers and landlords are achieving great results right now as stock levels are low due to the sustained high demand”. The average sales price is now R2.835 million.

Mixed-use neighbourhoods are generally highly sought by investors for high rental demand and stable yields, said Seeff. They often boast a high percentage of residential rental investments with yields of 7-10%. V&A Waterfront is lower at around 4-6% due to the high average prices.

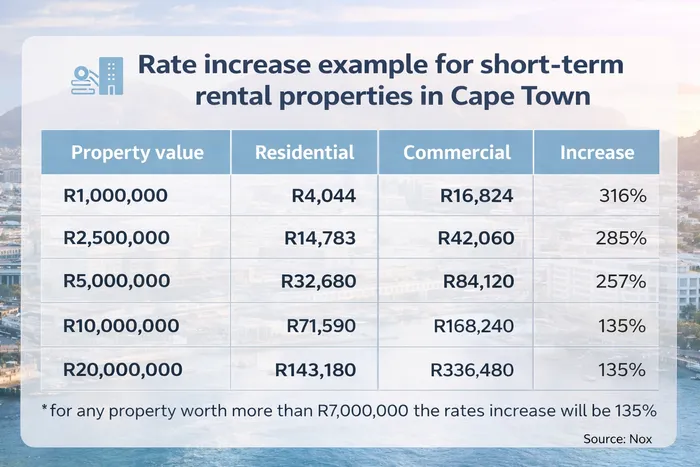

However, new cost pressures are emerging in that same market.

Proposed changes by the City of Cape Town could see short-term rental properties that are not primary residences reclassified from residential to business or commercial tariffs, according to Nox Cape Town.

This could increase rates by as much as 135%. For property owners, that would translate into significant cost increases.

“For property owners who rely on rental income – whether as supplementary revenue, pension income, or portfolio investment returns – understanding what these proposed changes could mean for net yields is essential,” said Nox.

Rate hikes in Cape Town will affect landlords.

Image: ChatGPT with Nox data

At R1 million, annual rates could rise from R4,044 to R16,824. At R5 million, they could increase from R32,680 to R84,120, based on Nox modelling.

These costs apply regardless of occupancy, directly affecting net yield and cash flow, particularly during shoulder and winter months when margins are already tighter, the firm said. For many properties, this could result in an additional expense of between 4.5% and 6.5% of revenue.

The impact is likely to be most significant for mid-market properties between R2 million and R7 million, where the loss of the residential rebate further increases costs.

At the same time, demand is shifting towards higher price brackets, according to BetterBond.

“There is also a noticeable shift in market activity toward higher price brackets, with the share of homes above R2 million increasing meaningfully over the past two years. While the R500 000 to R1 million segment remains the most active, its relative share is declining, suggesting a gradual rebalancing of demand as interest rates ease,” said Potgieter.

First-time buyers remain a key driver of activity, says Samuel Seeff, chairman of the Seeff Property Group. They account for between 46% and 48% of purchases nationally, supported by lower interest rates and competition among banks.

In Gauteng metros such as Johannesburg and Tshwane, they make up around 41% of activity, with price ranges between R1 million and R1.3 million offering accessible entry points, Seeff said.

In lower-priced regions such as North West, that share rises to as much as 52%. In the Western Cape, higher average prices – typically between R1.5 million and R1.8 million – reduce first-time buyer participation to around 36%, according to Seeff.

Policy support continues to underpin this segment. The transfer duty exemption threshold of R1.21 million reduces upfront costs, while government subsidies and 100% home loans support entry-level buyers, Seeff said.

Recent budget changes, including the increase in the capital gains tax exclusion on the sale of a primary residence from R2 million to R3 million, may provide additional support to the housing market, according to BetterBond.

IOL BUSINESS