From unpaid bills to workplace burnout, financial stress is reshaping how South Africans live, work and plan for the future.

Image: File photo

South Africans are under growing financial pressure, with more households struggling to pay bills, take on debt and cope with rising living costs.

The strain is not just financial but is increasingly affecting how people live, work and plan for the future.

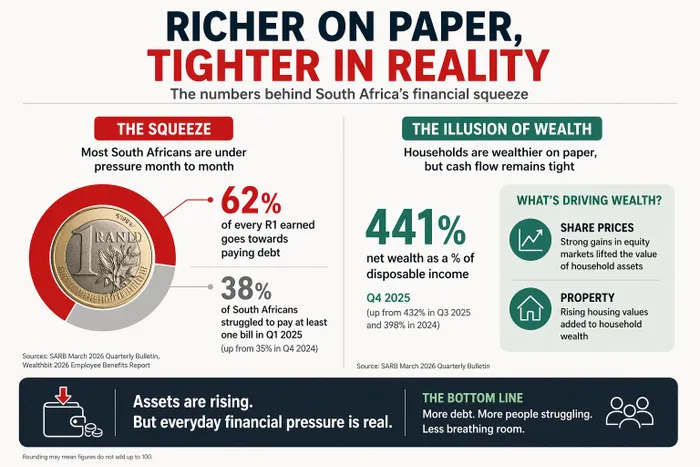

Data from fintech company Wealthbit shows that 38% of South African consumers struggled to pay at least one bill in the first quarter of 2025, up from 35% in the previous quarter. At the same time, 70% of workers across Africa are living from paycheck to paycheck.

Household debt remains high, with the South African Reserve Bank’s debt-to-income ratio showing that South Africans have to put 62c of every R1 they earn towards paying debt, a significant portion of income that is already committed before the month even begins.

Financial vulnerability is also spreading beyond lower-income groups. Nearly 29% of emerging high-income earners have no emergency savings, highlighting how even relatively well-paid households are struggling to build financial buffers.

Richer on paper, tighter in reality.

Image: ChatGPT

This pressure is beginning to change behaviour. Applications for debt counselling have risen sharply, with many consumers turning to credit, dipping into retirement savings or restructuring debt to stay afloat, says National Debt Counselling Association.

“The reality is that we’re going to see people borrowing more,” notes National Debt Counselling Association chairperson René Moonsamy.

While credit can be useful, it becomes risky when it is used to fund everyday expenses or repay existing debt, the association explains. In those cases, borrowing can create a cycle that becomes increasingly difficult to break.

Moonsamy defines ‘good’ credit as being affordable, well-managed and used for productive purposes that improve your long-term financial stability. “For example, buying a car to get to work or generate an income, furthering your education or paying for a renovation to add value to your house.”

Payments should be affordable relative to income, and the interest rates should be in line with a consumer’s risk profile. Making payments on time allows you to build a positive financial record, making it possible to access financial products at better rates, because your credit score shows you are financially reliable, says the association.

‘Bad credit,’ Moonsamy explains, is unaffordable, high-cost or poorly managed borrowing, usually for short-term consumption that adds no lasting value. Examples include using credit to fund lifestyle or basic living expenses, or taking new credit to repay old loans.

“There’s nothing inherently wrong with credit. It’s integral to a functioning economy. What’s important to understand is whether it benefits you or not,” says Moonsamy.

One of the biggest issues is not necessarily overspending, but a lack of visibility. Arrie Pieterse, head of product at Wealthbit, said many consumers simply do not have a clear picture of where their money is going. “Buying on credit usually makes that purchase more expensive over time, especially once interest is added,” he adds.

In many cases, consumers pay only the minimum on outstanding balances, leaving them trapped in debt for far longer than expected, says Pieterse.

“Money is one of the biggest sources of stress in people’s lives,” says Alex Cook, chief executive of Wealthbit. The impact of financial stress is not confined to household budgets increasingly spilling into the workplace.

Financially stressed employees are more likely to miss work, lose focus or look for new jobs, affecting both productivity and performance.

Presenteeism, where employees are physically present but mentally distracted, can result in a loss of more than 27 working days a year, while financially stressed workers take more sick leave than their peers, says Wealthbit citing research such as that undertaken by PwC.

According to Gary Kayle, CEO of Worth, Cumulate’s financial education brand, “financial stress goes far beyond numbers on a bank statement. When money problems extend beyond budgets and are left unaddressed, they begin to affect mental health, focus, as well as personal and work relationships. It affects your happiness levels”.

Jaco Prinsloo, a financial adviser at Alexforbes, says most mid-career professionals do not fail because of big, reckless decisions. “Instead, they drift into small, reasonable choices that compound over time,” he notes.

Among the “mistakes” that professionals make is delaying retirement planning, says Prinsloo. “The real cost of delaying is not just time, but the loss of compounding – starting even a decade later often means you need to contribute significantly more to reach the same outcome,” he says.

Another flag Prinsloo points to is when a lifestyle upgrade becomes a form of inflation. “Over time, what once felt like a luxury becomes normal and expenses quietly rise to match income. This can leave you earning more but not feeling financially ahead,” he says, noting that a structured approach to investing can help with this dilemma.

Prinsloo also highlights the risk of being underinsured as insurance is often treated as a cost rather than a financial strategy. “It is frequently overlooked or left unchanged for years.

Many professionals assume employer-provided cover is sufficient, but it is rarely aligned with their actual responsibilities,” he adds, speaking to the need to protect income and ensure that financial obligations can be met.

Dr Avron Urison, Chief Medical Officer at 1Life Insurance, explains that “financial protection is not a luxury; it is a cornerstone of a resilient and sustainable life”.

As Worth puts it: “While wealth itself may not guarantee happiness, understanding how to manage money can make life significantly less stressful.”

PERSONAL FINANCE