Discover how Finance Minister Enoch Godongwana's latest Budget Speech offers unexpected relief for South African consumers, with significant changes to tax brackets and savings incentives.

Image: GCIS

Finance Minister Enoch Godongwana’s Budget Speech to Parliament on Wednesday was brighter than generally expected and a welcome turnaround from last year’s fiasco, when the Minister unilaterally tried to increase VAT without buy-in from the other parties in the Government of National Unity.

I think we can safely say that since then the other parties have had greater influence on our country’s financial planning.

But the economic environment has also changed radically. Last year the government was desperately searching for ways to raise revenue, whereas this year, thanks to the commodity-boom windfall (largely of US President Donald Trump’s making, I would suggest), the government is now able to offer some relief to taxpayers.

Well, not relief exactly.

Taxpayers won’t be paying less tax in most instances; they just won’t be paying more. And through boosted incentives for long-term savings, they will hopefully be encouraged to save more.

Hayley Parry, head of financial education at financial education provider Worth, says the Minister delivered a Budget that was “stability-focused with a strong leaning towards correcting consumer-based pain points that have hurt both the bank accounts and future financial standing of South Africans.

“Government has withdrawn the previously proposed R20 billion in tax increases. There is no VAT hike and no broad-based income tax shock. That protects disposable income at a time when households are already stretched. Personal income tax brackets and rebates have been fully adjusted for inflation, after two years of no inflationary-linked adjustments. This prevents ‘bracket creep’, where people pay more tax simply because of inflationary salary increases. It protects take-home pay, particularly for middle-income earners,” Parry says.

Jurgen Eckmann, wealth manager at Consult by Momentum, says the Budget was largely consumer-friendly. “Consumers will be cheering about some relief provided in the form of a full inflation adjustment to personal income tax brackets, while the increase in the tax-free savings account (TFSA) limit and the higher retirement fund deduction cap meaningfully expand tax-efficient saving capacity. For those able to use these tools, this is one of the more favourable savings environments in recent years,” Eckmann says.

The Minister’s announcements were also small-business friendly, raising the turnover threshold beneath which these businesses don’t have to register for VAT from R1 million to R2.3 million and upping the turnover tax threshold by the same amount.

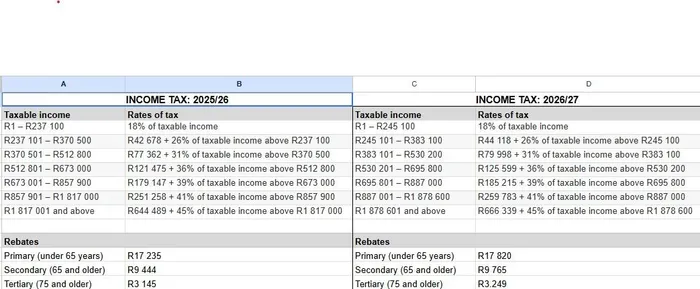

For consumers, apart from changes to the income tax brackets (see table) and retirement savings and TFSA thresholds, there were adjustments to capital gains tax (CGT), donations tax and medical tax credits.

I was disappointed that there were no increases in the exemptions for interest income, which remain at R23 800 for individuals under 65 years and R34 500 for those aged 65 and older.

For consumers, apart from changes to the income tax brackets and retirement savings and TFSA thresholds, there were adjustments to capital gains tax (CGT), donations tax and medical tax credits.

Image: Supplied.

All brackets have been adjusted upwards by about 3.4%, roughly the current inflation rate (see table). This means that if your income has risen by inflation, you will not be paying a greater percentage of it to the taxman, as may have been the case in previous years. You pay no tax if you are under 65 and your taxable income is less than R99 000 (up from R95 750). If you are between 65 and 75 that figure is R153 250 (up from R148 217), and if you are 75 or older, the threshold is R171 300 (up from R165 689).

The annual CGT exclusion for individuals rises from R40 000 to R50 000. The exclusion in the year of death increases from R300 000 to R440 000 (this was last increased in 2017). The exclusion on the disposal of a primary residence increases from R2 million to R3 million (this has not increased since 2012).

With much talk recently of abolishing medical tax credits entirely, the Minister surprisingly raised the tax credits for medical scheme contributions to adjust for inflation, from R364 to R376 per month for the main member and first dependant and from R246 to R254 for each additional dependant. Credits for out-of-pocket medical expenses remain unchanged.

The rates of donations tax have not changed (20% on the first R30 million and 25% on amounts above that), but the exemption limit has increased from R100 000 to R150 000 per year. This was last increased in 2007.

PERSONAL FINANCE