Finance Minister Enoch Godongwana delivered a National Budget on Wednesday that landed meaningful wins for consumers, savers and small businesses.

Image: Parliament

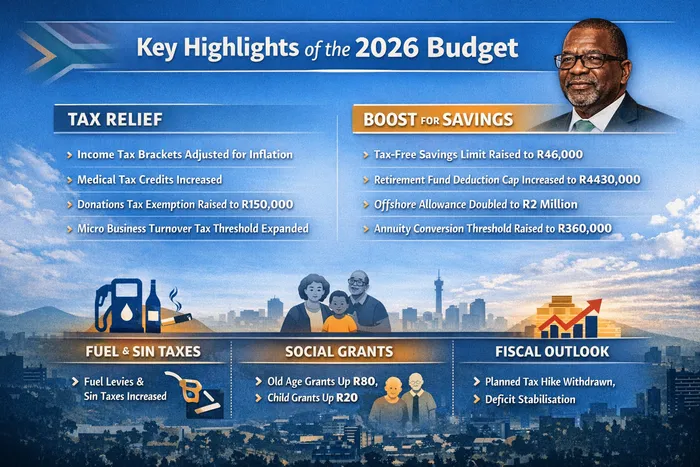

Delivering an upbeat National Budget on Wednesday, Finance Minister Enoch Godongwana provided much-needed relief to consumers in the form of inflation-adjusted tax brackets, higher tax-free savings limits, and expanded retirement contribution thresholds.

Yael Geffen, CEO of Lew Geffen Sotheby's International Realty, says “this wasn’t just a budget; it was an acknowledgment that the engine of this country is its people and its businesses”. Godongwana “put money back into the pockets of households at a time when they need it most,” she says.

The minister delivered a stability-focused National Budget aimed at addressing consumer pain points, says Hayley Parry, co-founder of Cumulate and head of financial education at Worth. “It avoids major tax shocks, protects social spending and nudges South Africans toward greater savings,” she adds.

Although Darren Britz, partner and head of Legal at Tax Consulting SA and Richan Schwellnus, senior tax attorney at Tax Consulting SA, say that the day itself may have lacked drama, it actually delivered a series of quietly positive tax developments.

“Rather than introducing aggressive new revenue collection measures, National Treasury opted for stability, targeted relief and structural adjustments that favour taxpayers, savers and small businesses,” they say.

Britz and Schwellnus point out that, in a year where additional tax increases of R20 billion had previously been pencilled in, the most notable policy decision was their withdrawal.

“This alone signals a meaningful improvement in fiscal confidence and a recognition that further tax pressure could have been economically counterproductive,” they say.

How National Budget 2026 affects average consumers.

Image: ChatGPT

Fixing bracket creep

Of particular note for most commentators was that there would be adjustments to income tax brackets for the first time in many years. Ester Ochse, FNB product head of Integrated Advice, says that these inflation-linked adjustments “does mean that there will be a bit of a relief coming to the consumer”.

Jurgen Eckmann, wealth manager at Consult by Momentum, says consumers will cheer the inflationary adjustment to personal income tax brackets, particularly after two years of bracket creep.

Yet, Parry notes that this breathing room “is not the same as financial progress. The smart move now is to use this stability to reduce debt or build up your emergency fund; not expand lifestyle costs”.

Britz and Schwellnus point out that lower and middle-income taxpayers stand to benefit the most from these adjustments, “reinforcing the progressive design of the tax system while providing some breathing room in a high cost-of-living environment”.

Lance Collop, CA (SA) and Chartered Tax Adviser, says the “2026 Budget marks a rare and welcome ceasefire in the war on the middle-class pocketbook”. He notes that remuneration threshold for tax-exempt bursaries has been raised to R900 000.

“This means more parents qualify for help with their children’s school fees, and more employees can be rewarded for their loyalty without the South African Revenue Service taking a massive cut. For the average taxpayer, this budget is a defensive win that finally allows their 2026 raises to stay in their bank accounts,” says Collop.

Collop adds that, by raising the 'remuneration proxy' for employer-provided housing loans from R250 000 to R360 000 – and increasing the eligible property market value to R650 000 – Treasury is finally acknowledging the reality of the current property market for lower-to-middle income earners.

Targeting savings

The minister also took direct aim at South Africa’s low savings rate, says Geffen.

“These are smart, targeted moves,” Geffen noted. “Encouraging people to save – and to save more – is exactly how you build a resilient economy. It’s a vote of confidence in our collective future.”

Adrian Hope-Bailie, Fynbos Money founder, welcomes the proposal to increase the annual tax-free savings account contribution limit from R36 000 to R46 000. “This long-awaited adjustment, the first in six years, is a critical step in helping South Africans protect their wealth from inflation,” he says.

Hope-Bailie points out that investors can now reach their R500 000 lifetime contribution cap roughly three years faster, allowing their capital more time to grow, entirely shielded from taxes on dividends, interest, and capital gains.

Ochse also notes that the retirement fund deduction cap rises from R350 000 to R430 000, the annuity conversion threshold increases to R360 000, and the living annuity commutation threshold moves to R150 000. In addition, she points out that the single discretionary offshore allowance has doubled to R2 million.

Eckmann says this is a Budget that rewards discipline. “The policy direction is constructive, but wealth creation will depend far more on proactive financial planning than on macro optimism alone,” he adds.

While the Budget includes some welcome changes that should improve consumers’ financial landscape, it does not eliminate cost-of-living pressures and so the real differentiator will be financial capability, says Parry.

Parry points towards the negative effects of fuel levies rising in line with inflation. “Higher petrol and diesel costs will filter through to transport, food and goods prices. This affects every consumer, directly or indirectly,” she says, noting that they hit lower income earners the hardest.

The general fuel levy will increase by 9 cents per litre for petrol and 8 cents per litre for diesel, while the Road Accident Fund levy will increase by 7 cents per litre.

“If households use tax stability to reduce debt, take advantage of tax-free savings vehicles, plan for fuel-driven inflation and make intentional consumption decisions, then this can be a year of consolidation and resilience. If not, it will simply feel like another year of financial pressure,” Parry adds.

PERSONAL FINANCE